Buying a home in 2025 is one of the most rewarding and sometimes overwhelming experiences you’ll ever have. With housing markets shifting and lending guidelines evolving, understanding the mortgage application process is key to making confident, informed decisions.

This guide walks you through each step of getting a mortgage in 2025 from pre-approval and loan processing to underwriting and closing so you know exactly what to expect along the way.

Step 1: Get Pre-Approved for a Mortgage

Before you start touring homes, getting pre-approved is essential. This helps you understand how much you can afford and signals to sellers that you’re a serious buyer.

What is Mortgage Pre-Approval?

A mortgage pre-approval is a lender’s official evaluation of your credit, income, and financial history to determine how much you can borrow. It’s more reliable than pre-qualification because your information is verified with documentation.

Documents You’ll Need:

To get pre-approved, prepare these items:

- Debt Details: Current loans, credit cards, alimony, or child support

- Photo ID: Driver’s license or government-issued ID and Social Security number

- Proof of Income: Recent pay stubs, W-2s, and tax returns

- Employment Verification: Employer contact details or verification letter

- Assets: Bank statements, retirement accounts, and investment info

- Credit Authorization: Permission for a credit check

Benefits of Pre-Approval

- Credibility with Sellers: Demonstrates to sellers that you are a serious buyer.

- Clear Budget Understanding: Helps you know your price range.

- Faster Closing: Streamlines the mortgage process once you find a home.

Pro Tip:

Lenders may ask for additional documentation based on your situation (like immigration status, recent job changes, or non-traditional income). It’s smart to have digital and physical copies ready.

Step 2: Find Your Home and Make an Offer

Once pre-approved, it’s time for the fun part house hunting. With a clear budget, you can focus on properties that align with your goals.

How to Make a Strong Offer in 2025

- Research comparable sales to determine a fair offer price

- Limit contingencies to strengthen your offer in competitive markets

- Add a personal letter to connect with the seller on an emotional level

Step 3: Apply for Your Mortgage

Once your offer is accepted, you’ll formally apply for the loan.

What Happens During the Application

You’ll submit your complete financial details and property information. Within three business days, your lender will send a Loan Estimate, which outlines:

- Loan amount

- Interest rate

- Estimated monthly payments

- Closing costs

This is your opportunity to review the terms and ask questions before moving forward.

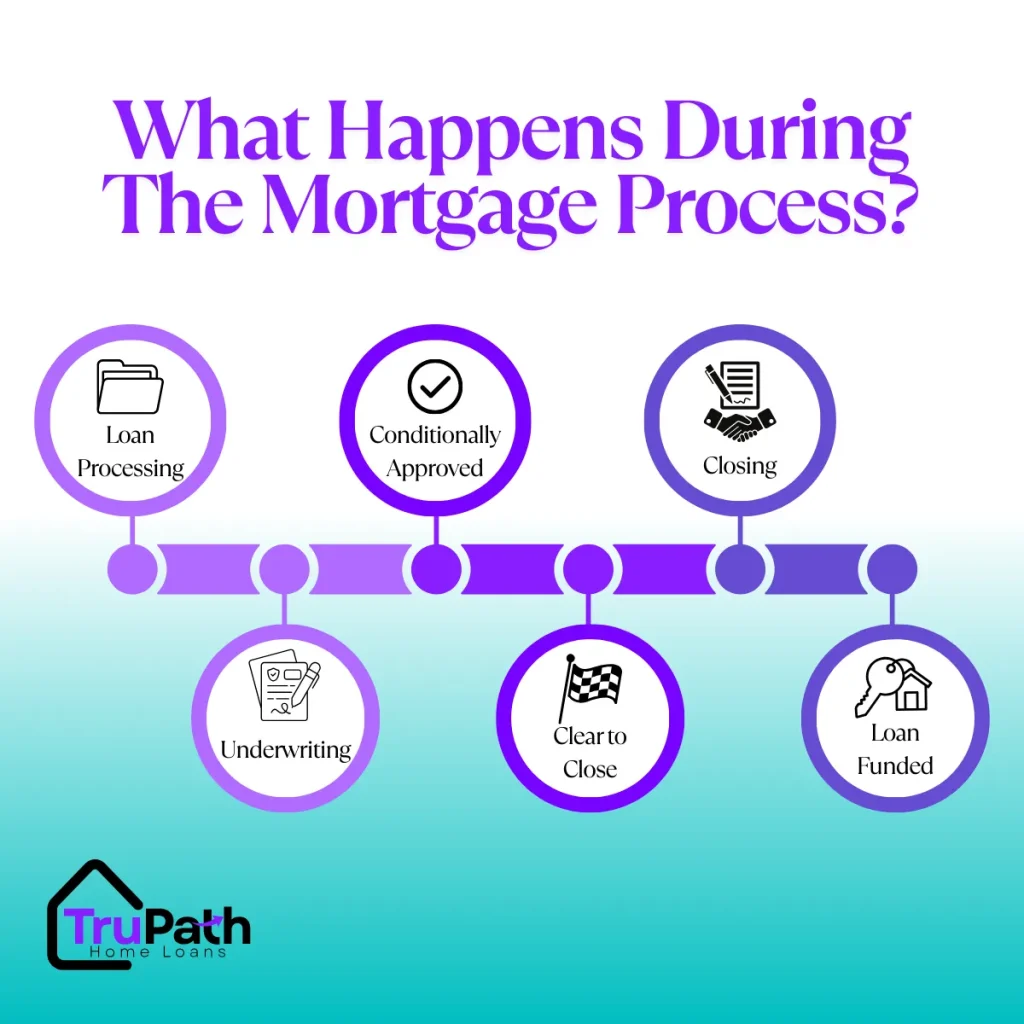

Step 4: Loan Processing

The lender’s processing team now verifies all information you provided to ensure everything matches your documentation.

What’s Included in Loan Processing

- Employment & income verification

- Appraisal: Confirms the property’s market value matches the loan amount

- Title search: Ensures the property is legally clear to sell

During this time, stay responsive to your lender missing documentation can delay the process.

Step 5: Mortgage Underwriting

Underwriting is the stage where the lender carefully evaluates your loan for risk and eligibility.

What the Underwriter Reviews

- Creditworthiness: Your credit history and score

- Debt-to-Income (DTI) ratio: Ensures your income supports your new mortgage

- Property details: Confirms the appraisal and condition

How Long It Takes

Underwriting can take anywhere from a few days to a few weeks, depending on the loan type and your financial complexity.

If your loan is approved congratulations! You’ll receive a “clear to close.”

Step 6: Closing on Your New Home

This is the final and most exciting step you officially become a homeowner!

What to Expect at Closing

- 3-Day Review: You’ll receive your Closing Disclosure at least three days before closing to review the final loan terms and costs.

- Final Walk-Through: Make sure the property’s condition matches the purchase agreement.

- Sign Documents: Once everything is verified, funds are transferred and the keys are yours!

Choosing the Right Mortgage Loan in 2025

Selecting the right loan type helps you save money and match your financial goals.

Fixed-Rate vs. Adjustable-Rate Mortgage

- Fixed-Rate Mortgage: Steady interest rate and predictable payments for the entire term

- Adjustable-Rate Mortgage (ARM): Lower initial rate that can change after a set period

Common Loan Programs

- Conventional Loans: Ideal for buyers with strong credit and stable income

- FHA Loans: Backed by the Federal Housing Administration; great for first-time buyers

- VA Loans: Exclusive to veterans and active-duty service members, often with no down payment

Mortgage Process FAQ

How Does the Housing Market Affect the Duration of the Underwriting Process?

In a competitive housing market, lenders may experience higher volumes of applications, potentially lengthening the underwriting process.

What Can Cause Delays in the Underwriting Process, and How Can These Be Avoided?

Common causes of delays include:

– Incomplete Documentation: Ensure all required documents are submitted promptly.

– Credit Issues: Address any credit report discrepancies before applying.

What Additional Steps Should a Self-Employed Individual or Business Owner Expect in the Underwriting Process?

Self-employed applicants may need to provide:

– Additional Income Verification: Tax returns for the past two years.

– Profit and Loss Statements: Recent statements to demonstrate business stability.

Conclusion

Understanding the mortgage application process in 2025 empowers you to navigate each step with confidence. By preparing thoroughly and working closely with your lender, you can streamline your journey to homeownership.

Disclaimer: This article is for educational purposes only and does not constitute financial or lending advice. Loan guidelines, limits, and eligibility requirements are subject to change. Always consult with a licensed mortgage professional to determine what loan options are best for your individual financial situation and homeownership goals.